Which ITR Form Should You Choose? Types & Eligibility Based on Income Type

60-Second Summary

- There are 7 ITR forms in India, and the correct one depends on your income type and taxpayer category.

- Salaried individuals with simple income up to ₹50 lakh usually file ITR-1.

- Individuals with capital gains, multiple properties, or foreign assets generally file ITR-2.

- Business owners and professionals maintaining books file ITR-3.

- Small taxpayers opting for presumptive taxation file ITR-4.

- Firms and LLPs file ITR-5, companies file ITR-6, and exempt trusts file ITR-7.

- Filing the wrong form can lead to defective return notices and delays.

- Reviewing income sources and eligibility carefully ensures smooth and compliant filing.

Many taxpayers either miss chances to save tax or end up paying penalties while filing. In FY 2023–24, over 8 crore Indians filed Income Tax Returns, yet that’s only about 6.68% of the population. So, what’s really going wrong? In many cases, it comes down to something basic; people simply don’t know which ITR form they should select. And that small confusion can lead to missed deductions, higher tax outgo, defective returns, or penalties for incorrect filing.

That’s exactly where Digilawyer helps. Their experts guide you on how to choose the right ITR form, applicable deductions, and the complete filing process, keeping it simple, clear, and stress-free.

What is Income Tax Return (ITR)?

ITR (Income Tax Return) is a form that taxpayers submit to the Income Tax Department to report their annual income, expenses, tax deductions, and taxes paid during a financial year. It is filed under the provisions of the Income Tax Act.

Filing ITR helps you:

- Claim tax refunds

- Carry forward losses

- Apply for loans and visas

- Maintain financial credibility

- Avoid penalties and legal notices

Even if your income is below the taxable limit, filing ITR can be beneficial for financial documentation and future compliance.

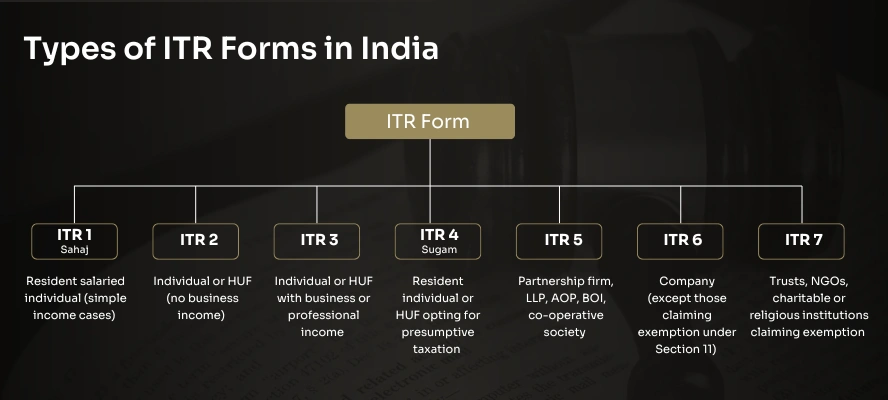

Types of ITR Forms in India

1. ITR FORM 1 (Sahaj)

Resident Individuals who fall under the following categories can opt for ITR-1 if total income is up to ₹50 lakh

Who Can and Cannot File ITR Form 1

Eligibility:

- Is a resident individual with total income not exceeding Rs. 50 Lakh during the Financial Year

- Income from Salary or Pension, or from one house property

- Income from Other Sources, such as interest from savings or FD (except winning a lottery or horse racing)

- Agriculture income less than Rs.5000

- If you have long -term capital gains up to Rs. 1.25 Lakhs from sources like interest from saving account, deposits, income tax refunds, family pension, and any other interest income.

- Income from tax refunds

- Family Pension

Not Eligible to file ITR-1:

- Total income over 50 Lakhs

- More than one house property.

- Income from business or profession

- Income from Foreign assets.

- If Long-term capital gains exceed Rs. 1.25 lakhs

- Directors or shareholders of unlisted companies.

- If invested in unlisted equity shares of a company

- Is an RNOR (Resident Not Ordinarily Resident) and NRI (Non- Resident)

- has tax deduction under section 194N of Income Tax Act

- If you have received ESOP shares from an eligible start-up employer

- is not covered under the eligibility conditions for ITR-1

2. ITR FORM-2

Individuals and HUFs (with no business income) who fall under the following categories can opt for ITR-2

Who Can and Cannot File ITR Form 2

Eligibility to file ITR-2

- Income exceeding the amount of Rs.50 Lakh

- Income received through salary, pensions, capital gains, and other sources (income received from sources other than business or profession)

- Income generated from foreign assets or destinations.

- Agricultural income exceeding Rs.5,000

- Income from multiple house properties that is more than Rs. 50 Lakh.

- Income from capital gains.

- Any investment made in unlisted shares

- Is an NRI, or RNOR.

- Is a director in a company

Not Eligible to file ITR-2

- If you have income from the profits and gains of a business or profession.

- If you are a company, LLP, OR Partnership Firm.

3. ITR FORM-3

Individuals and HUFs having “Business/profession income” should opt for ITR-3

Who Can and Cannot File ITR Form 3?

Eligible to file ITR-3

- Business or professional income requiring the maintenance of books of accounts and/or tax audit

- If you are running a proprietorship business like trading (F&O, intraday), manufacturing, retail, or e- commerce

- If you are a partner in a partnership firm or LLP and receive a salary, commission, bonus, or interest from the firm.

- If you are earning income from freelancing or consultancy

- If you have income from salary or pension, capital gains, rental income, or foreign income/assets

- You are not opting for presumptive taxation under Sections 44AD, 44ADA, or 44AE

Not Eligible to file ITR-3

- Individuals or HUFs are eligible to file ITR-1, ITR-1, or ITR-4.

- If you don’t have any business or professional income

4. ITR FORM-4 (Sugam)

Resident individuals, HUFs, and partnership firms (excluding LLPs) opting for presumptive taxation can file ITR-4 if total income is up to ₹50 lakh

Presumptive taxation scheme- This scheme allows small taxpayers, including individuals, HUFs, and partnership firms (not LLPs), to calculate and pay the tax on a fixed percentage of their turnover or gross receipts.

Who Can and Cannot File ITR Form 4?

Eligible to file ITR-4

- If you have business income under Section 44D or 44E (presumptive basis)

- If you have professional income under Section 44ADA

- Salary or pension income up to ₹50 lakh

- Income from one house property (with total income not exceeding ₹50 lakh and no loss carry forward)

- Income from other sources, not more than ₹50 lakh (excluding lottery or racehorse winnings)

- Freelancers earning from eligible professional services can also opt for this form if their gross receipts are under Rs. 50 Lakh, and they choose presumptive taxation.

Not Eligible to File for ITR-4

- If your total income is more than Rs.50 Lakh.

- If you earn from more than one house property

- If you own foreign assets or hold signing authority in overseas bank accounts

- If you are a Non-Resident (NR) or Resident but Not Ordinarily Resident (RNOR)

- If you earn any foreign income

- If you are a director in a company

- If you have invested in unlisted equity shares

- If you are assessable on another person’s income

- If tax has been deferred on Employee Stock Ownership Plans (ESOPs)

- If you have any brought forward losses or need to carry forward losses

5. ITR FORM-5

Firms, LLPs, associations, and similar entities should opt for ITR FORM-5.

Who Can and Cannot File ITR Form 5?

Eligible to file ITR-5

- Partnership firm

- Limited Liability Partnership (LLP)

- Association of Persons (AOP)

- Body of Individuals (BOI)

- Society registered under the Societies Registration Act

- Local authority

- Artificial Juridical Person (AJP)

- Business trust or investment fund

- Estate of deceased person

- Estate of insolvent person

- Co-operative society

Not Eligible to file ITR-5

- Individual

- Hindu Undivided Family (HUF)

- Company (required to file ITR-6)

- Trust, political party, charitable or religious institution required to file ITR-7

6. ITR FORM-6

For companies that are not claiming any exemptions under section 11 of the Income Tax Act, and are filed exclusively online, companies must submit this return with a digital signature.

Who Can and Cannot File ITR Form 6?

Eligible to file ITR-6

- Company registered under the Companies Act

- Private limited company

- Public limited company

- One Person Company (OPC)

- Foreign company taxable in India

- Company earning income from business or profession

- Company not claiming exemption under Section 11

Not Eligible to File ITR-6

- Individual

- Hindu Undivided Family (HUF)

- Partnership firm

- Limited Liability Partnership (LLP)

- Association of Persons (AOP)

- Body of Individuals (BOI)

- Trust, charitable or religious institution claiming exemption under Section 11 (required to file ITR-7)

7. ITR-7 FORM

ITR-7 is for trusts, charitable/religious institutions, and organizations that claim tax exemptions under specific sections of the Income Tax Act.

Who Can and Cannot File ITR Form 7?

Eligible to file ITR-7

- Trust claiming exemption under Section 11 or Section 12

- Charitable trust

- Religious trust

- Political party

- Scientific research association

- News agency

- Educational institution claiming exemption

- Hospital or medical institution claiming exemption

- University or other institution claiming exemption

- Business trust required to furnish return under specific provisions

Not Eligible to file ITR-7

- Individual (unless filing as trustee of eligible trust)

- Hindu Undivided Family (HUF)

- Partnership firm

- Limited Liability Partnership (LLP)

- Company not claiming exemption under Section 11 (required to file ITR-6)

- AOP or BOI not covered under ITR-7 provisions

How to Choose the Right ITR Form Based on Different Factors?

Choosing the correct ITR form depends on your income type, taxpayer category, and tax scheme. Here’s how you can decide:

1. Based on Type of Taxpayer

- Individual (salaried or non-business income) - ITR-1 or ITR-2

- Individual with business or professional income - ITR-3 or ITR-4

- HUF with non-business income - ITR-2

- HUF with business income - ITR-3

- Partnership firm or LLP -ITR-5

- Company - ITR-6

- Trust or institution claiming exemption - ITR-7

2. Based on Source of Income

- Salary, one house property, and income up to ₹50 lakh - ITR-1

- Salary, capital gains, multiple properties, foreign assets - ITR-2

- Business or professional income (regular books maintained) - ITR-3

- Business under presumptive taxation (Sections 44AD, 44ADA, 44AE) - ITR-4

3. Based on Business Structure

- Proprietorship - ITR-3 or ITR-4

- Partnership firm or LLP - ITR-5

- Private limited or public limited company - ITR-6

4. Based on Exemption Status

- Charitable or religious trust claiming exemption - ITR-7

- Company not claiming exemption under Section 11 - ITR-6

5. Based on Residential Status

- Resident individual - ITR-1, 2, 3, or 4 depending on income

- Non-resident with capital gains or foreign assets - Usually ITR-2 or ITR-3

Simple rule:

First identify who you are (individual, firm, company, trust), then check your income sources (salary, capital gains, business, presumptive), and finally select the matching ITR form.

Common Mistakes While Choosing ITR Forms

Here are the most frequent errors taxpayers make:

🚫 Choosing ITR-1 Despite Having Capital Gains: Many salaried individuals file ITR-1 without reporting capital gains from shares, mutual funds, or property. If you have capital gains, ITR-2 or ITR-3 may apply instead.

🚫 Filing ITR-2 Instead of ITR-3: If you have business or professional income (like freelancing, consulting, or proprietorship income), you cannot file ITR-2. You must file ITR-3.

🚫 Confusing ITR-3 and ITR-4: ITR-4 applies only if you opt for presumptive taxation under Sections 44AD, 44ADA, or 44AE. If you maintain regular books of accounts, you should file ITR-3.

🚫Ignoring Foreign Assets or Income: Residents with foreign income or foreign assets cannot file ITR-1. They must file ITR-2 or ITR-3.

🚫 Companies or LLPs Filing Wrong Forms: LLPs must file ITR-5, while companies (other than those claiming exemption under Section 11) must file ITR-6.

🚫 Not Checking Eligibility Conditions: Many taxpayers assume eligibility without reviewing turnover limits, income ceilings, or exemption conditions.

Process to Choose the Correct ITR Form

Follow this step-by-step approach:

Step 1: Identify Your Taxpayer Category

Are you an individual, HUF, partnership firm, LLP, company, or trust?

Step 2: Identify Your Income Sources

Check whether you earn from:

- Salary or pension

- House property

- Capital gains

- Business or profession

- Presumptive taxation

- Foreign income

Step 3: Check Presumptive Scheme Eligibility

If your business turnover falls within limits and you opt for presumptive taxation, ITR-4 may apply.

Step 4: Review Exemption Status

Charitable trusts, political parties, and exempt institutions may need to file ITR-7.

Step 5: Cross-Verify Before Filing

Always double-check eligibility criteria before submitting your return.

Requirements Before Choosing an ITR Form

- Keep these ready before selecting your form:

- PAN and Aadhaar details

- Form 16 (for salaried individuals)

- Business financial statements (if applicable)

- Capital gains statements

- Bank statements

- Details of foreign assets or income

- Turnover and profit details (for business owners)

- GST registration details (if applicable)

Having accurate information prevents incorrect form selection.

Tips & Best Practices

- Don’t ever opt for a simpler form because you want to save time.

- Don’t miss reporting any sources of income, no matter how small.

- Match income with AIS and Form 26AS.

- Ensure you understand the turnover review and presumptive eligibility.

- File before the due date to avoid penalties and income tax notice.

- If unsure, consult a professional CA

Correct form selection ensures faster processing and avoids defective return notices.

Why Choose DigiLawyer for Your Income Tax Return?

Filing your Income Tax Return (ITR) doesn’t have to be stressful, and with DigiLawyer, it won’t be. We make the process easy, accurate, and tailored to your needs.

Expert Guidance: Receive expert advice to understand taxes, your obligations, and the best approach for individuals and businesses.

Tax Planning: Get strategies to maximize deductions, reduce tax liability, and plan effectively for future savings with our tax planning guidance.

Convenience: File your ITR from the comfort of your home, anytime, without the hassle of paperwork or long office visits. We handle everything online for a smooth experience.

Accurate & Compliant: We keep up with the latest tax laws to ensure your filing is fully compliant and penalty-free.

Secure: Your financial data is safe with us. We use advanced security measures to protect your information.

Faster Refunds: With our seamless e-filing process, your ITR acknowledgment is quick, and you can easily track your refund status.

Ongoing Support: From document collection to post-filing queries, we are here to guide you at every step.

Conclusion

Choosing the right ITR form for FY 2025–2026 is not just about compliance, it directly impacts refund processing, tax liability, and your overall financial record. A small mistake in selecting the wrong form can result in notices, penalties, or delayed refunds. With multiple eligibility conditions, income categories, and exemption rules, it’s easy to get confused especially if you have capital gains, business income, foreign assets, or are opting for presumptive taxation.

Instead of taking risks, let experts handle it. DigiLawyer’s experienced CA team carefully evaluates your income profile, selects the correct ITR form, ensures accurate reporting, and files your return on time securely and stress-free.

FAQs on Different Types of ITR Forms

Can I file ITR if I have no income?

Yes, you can file a Nil return even if you have no taxable income. It helps maintain financial records and may be useful for visa or loan purposes.

Is it mandatory to file ITR if tax is already deducted (TDS)?

Yes. Even if TDS is deducted by your employer or bank, you must file ITR if your income exceeds the basic exemption limit or if you meet specified conditions.

What is a defective return notice?

If you file the wrong ITR form or provide incomplete information, the Income Tax Department may mark your return as defective and ask you to correct it within a specified time.

Can I switch from old tax regime to new tax regime while filing ITR?

Yes, individuals without business income can choose between old and new regimes each year. Business taxpayers have certain restrictions.

What happens if I miss the ITR filing deadline?

You can file a belated return within the allowed time by paying a late filing fee and interest, if applicable.

Can I revise my ITR after filing?

Yes, you can file a revised return before the prescribed deadline if you discover mistakes or omissions.

Do I need to file ITR if my income is below ₹2.5 lakh?

It may not be mandatory, but filing is advisable for documentation, refunds, or if you meet specific high-value transaction criteria.

Is Aadhaar mandatory for filing ITR?

Yes, linking Aadhaar with PAN is mandatory for filing ITR in most cases.

How long does it take to get an ITR refund?

Refund timelines vary, but accurate and properly verified returns are generally processed faster.

What is AIS and why should I check it before filing?

AIS (Annual Information Statement) contains details of your financial transactions. Reviewing it helps ensure accurate reporting of income.

Can I file ITR without Form 16?

Yes, you can file ITR using salary slips, bank statements, and Form 26AS if Form 16 is unavailable.

Is GST registration required to file ITR?

No. GST registration and ITR filing are separate compliances, though business income details may be linked.

Do freelancers need to file ITR?

Yes. Freelancers must file ITR if their income exceeds the basic exemption limit or if they wish to claim refunds or carry forward losses.

Can NRIs file ITR online?

Yes, NRIs can file ITR online depending on their income earned or accrued in India.

- What is Income Tax Return (ITR)?

- Types of ITR Forms in India

- Who Can and Cannot File ITR Form 1

- Who Can and Cannot File ITR Form 2

- Who Can and Cannot File ITR Form 3?

- Who Can and Cannot File ITR Form 4?

- Who Can and Cannot File ITR Form 5?

- Who Can and Cannot File ITR Form 6?

- Who Can and Cannot File ITR Form 7?

- How to Choose the Right ITR Form Based on Different Factors?

- 1. Based on Type of Taxpayer

- 2. Based on Source of Income

- 3. Based on Business Structure

- 4. Based on Exemption Status

- 5. Based on Residential Status

- Simple rule:

- Common Mistakes While Choosing ITR Forms

- Process to Choose the Correct ITR Form

- Step 1: Identify Your Taxpayer Category

- Step 2: Identify Your Income Sources

- Step 3: Check Presumptive Scheme Eligibility

- Step 4: Review Exemption Status

- Step 5: Cross-Verify Before Filing

- Tips & Best Practices

- Why Choose DigiLawyer for Your Income Tax Return?

- Conclusion

- FAQs on Different Types of ITR Forms

How to Claim HRA While Filing ITR: Eligibility, Calculation & Documents

Learn how to claim HRA correctly, calculate your exemption, prepare the required documents, and avoid common mistakes when filing your Income Tax Return.

Difference Between Tax Evasion, Tax Avoidance and Tax Planning

Tax planning, tax avoidance, and tax evasion may sound similar, but their legality and consequences are completely different. Here’s a simple breakdown of what is legal, risky, and illegal.

5 Ways to Save Income Tax in New Tax Regime (FY 2025-26)

The new tax regime offers lower tax rates, but saving money now depends on your salary structure. Here’s what you need to know to reduce your tax.

Disclaimer: DigiLawyer is not a law firm, a substitute for a lawyer or law firm, a chartered accountancy firm, or a company secretary firm. We act solely as an intermediary between users and registered professionals, and also offer AI-powered legal assistance, consultation, and document drafting tools to improve access to legal support. Use of our website, services, or AI tools is at the sole risk of the user and does not create any lawyer-client or professional relationship. All consultations and interactions facilitated through our platform are strictly between the user and independent professionals. DigiLawyer is not liable for any actions, decisions, or outcomes arising from the use of our platform, AI tools, or reliance on any advice, consultation, or content provided by us or third-party professionals.

Use of our products and services is subject to our Privacy Policy & Terms of Service