ITR Filing Last Date for FY 2025-26 (AY 2026-27)

60-Second Summary

- Unsure about the exact last date to file your ITR for FY 2025-26? The deadline may not be the same for everyone, and missing it can be costly.

- Many taxpayers assume they have more time than they do. A small misunderstanding about due dates can lead to penalties, interest, and unnecessary stress.

- What really happens if you miss the deadline? Is there still a way to file? And how much could it cost you?

- Filing late is not just about paying a small fee it can impact refunds, future tax benefits, and even your financial credibility.

- There are multiple options available if you delay, but each comes with specific conditions and consequences you should know.

- Simple mistakes like waiting for extensions, not verifying your return, or misunderstanding your category can create bigger compliance issues.

Introduction

Many taxpayers wait until the last moment to file their Income Tax Return, assuming they still have time. Others believe the deadline is the same for everyone. But what if your actual due date is different? What if missing it by even a single day leads to penalties, interest, or loss of important tax benefits?

The confusion around ITR deadlines often results in unnecessary stress, late fees, delayed refunds, and compliance issues. Questions like “Can I still file after the due date?” “What happens if I miss 31st July?”, or “Will there be an extension?” This leaves many people unsure about the right next step.

This blog clears that confusion. You’ll understand the exact last dates for different categories of taxpayers, what happens if you miss them, the penalties involved, and the options still available to you. And if you want to avoid last-minute panic altogether, DigiLawyer’s tax experts ensure your ITR is filed accurately and on time, making the entire process simple, guided, and stress-free.

What Is the Deadline For Filing Income Tax Return (FY 2025-2026)?

The due dates for filing ITR for FY 2025–26 (AY 2026–27) vary based on the type of taxpayer. Below is a brief overview.

Category of Taxpayer | Due Date for Tax Filing - FY 2025-26 *(unless extended) |

ITR-1 & ITR-2 | 31st July 2026, usually extended till mid-Sept. |

ITR-3 & ITR-4 (non-audit cases) | 31st August 2026 |

ITR-3 & ITR-4 (Requiring Audit) | 31st October 2026 |

Businesses requiring transfer pricing reports (in case of international/specified domestic transactions) | 30th November 2026 |

Revised return | 31st March 2027 |

Belated/late return | 31st December 2026 |

Updated return | 31 March 2031 (4 years from the end of the relevant Assessment Year) |

- The last date for the income tax return in India is 31st July for individuals filing ITR-1 and ITR-2.

- The deadline for non-audit taxpayers mandated to submit ITR-3 and ITR-4 is August 31, 2026,

- And for individuals who require an audit is October 31, 2026.

Nonetheless, should you fail to meet this deadline, you may submit a late return by 31 December 2026; however, late filing penalties and interest will be incurred.

What Happens If You Miss the Due Date to File ITR

Missing the due date of filing your ITR can have both financial and legal consequences. Here’s a clear breakdown of what happens if you forget the date.

1. Late filing fees (Section 234F)

If you miss the original due date, a fine of Rs. 5000 will be imposed if your income exceeds 5 lakhs. And if the income is up to Rs. 5 lakh, the fine is Rs. 1000. This fee will be charged after the due date, until December 31st. These fees will be charged only one time, and not as a monthly charge.

2. Interest on Tax Due (Section 234A)

You may also be required to pay interest if you fail to file it on time. Interest is imposed at 1% per month or part of a month on the outstanding balance beginning the day after the due date.

3. Risk of Notice from the Income Tax Department

If you don’t file at all and your earning exceeds the basic exemption limit, you may receive a notification, or in serious circumstances, the Income Tax department may send a notice.

Know more: Common Income Tax Notices Salaried Employees Receive

We can also give you a Real-life example of our client, Mr Ram and how Digilawyer helped them with their problem.

Mr Ram had:

- Annual Income: ₹9,20,000

- Tax still payable: ₹40,000

- Filed a return 3 months late

Calculation:

Late Filing Fee: ₹5,000 (income above ₹5 lakh)

Interest: ₹40,000 × 1% × 3 months = ₹1,200

Total Extra Amount Paid:

- Late Fee: ₹5,000

- Interest: ₹1,200

- Total Penalty: ₹6,200

He had to pay ₹46,200 (₹40,000 tax + ₹6,200 extra).

How DigiLawyer Helped-

Mr Ram approached DigiLawyer after missing the deadline. Our experts calculated the exact penalty, reviewed his deductions, corrected errors, and filed his belated return properly, ensuring no further notices or compliance issues.

If you’ve missed your ITR deadline, acting early can save you from bigger penalties later.

👉 Please note that the above points are for individuals and businesses both, but some scenarios could be different for businesses, like-

- Penalty- A fine of Rs. 10,000 could be charged for late filing under the section 234F of the IT Act.

- Prosecution- In severe cases, the company may be prosecuted for non-compliance, leading to imprisonment of up to 7 years and/or fines.

- Disqualification of Directors- The company’s director may be disqualified from acting as an appointed director for another company.

- Loss of government contracts- The company may be disqualified from taking any official contracts.

What Is the Next Step to Take If You Miss the Deadline?

Now, let’s talk about the next measures one can take to file the income tax return-

Step 1: File a Belated Return

If you missed the original due date (usually 31st July):

- You can file a Belated Return

- Deadline: 31st December of the relevant assessment year

- Late filing fee under Section 234F will apply

- Interest under Section 234A (1% per month) will apply

This is the most common solution if you are only a few months late.

Step 2: File an Updated Return

If you missed both the original and belated deadlines:

- You can file an Updated Return (ITR-U)

- Allowed within 4 years from the end of the relevant assessment year

- For example: For FY 2025–26 (AY 2026–27), the updated return can be filed up to 31 March 2031.

- You can file it whether you previously filed an ITR.

Important points to remember:

- You cannot claim new refunds or additional benefits

- Additional tax and penalty will apply

- An updated return cannot be revised again

The longer you delay, the higher the financial burden due to interest and penalties. Filing at the earliest helps reduce compliance risks.

Consequences of Missing the ITR Filing Deadline

Here are some consequences you can face if you miss the ITR filing deadline-

- High Interest- If you file your return after the deadline, you will be required to pay interest at the rate of 1% each month or part month on the unpaid tax amount under Section 234A.

- Penalty fees- For failing to file ITR, you must pay a penalty of Rs 5000 for an individual having income more than 5 lakh, and Rs.1000 for upto 5 lakh income.

- Carry Forward Losses- If you fail to meet the deadline, there is a loss of carry-forward benefits. You cannot carry forward business losses, capital losses, or any speculation losses as well. This can impact your future tax planning and increase the tax burden on you. It’s better to consult for tax expert.

- Delay in Tax Refund- One consequence is a delay in the refund processing. Let’s suppose you were getting a refund on the total tax, but due to filing late, the refund will be delayed, and it could also happen that the refund may be reduced or denied. This will affect your compliance record and financial profile.

- Legal Prosecution- In some extreme cases, like tax evasion, there could be charges pressed which could lead to imprisonment from 3 months to 7 years, monetary fines, and confiscation of personal assets.

- Loss of credibility- Income tax return acts as proof for bank loans, is needed in documents for visa processing, and is proof for high-value transactions. Missing the deadline and filing late can lead to reduced credibility with the bank, which can affect your future possibility of taking loans from the bank, and may create issues in immigration documentation.

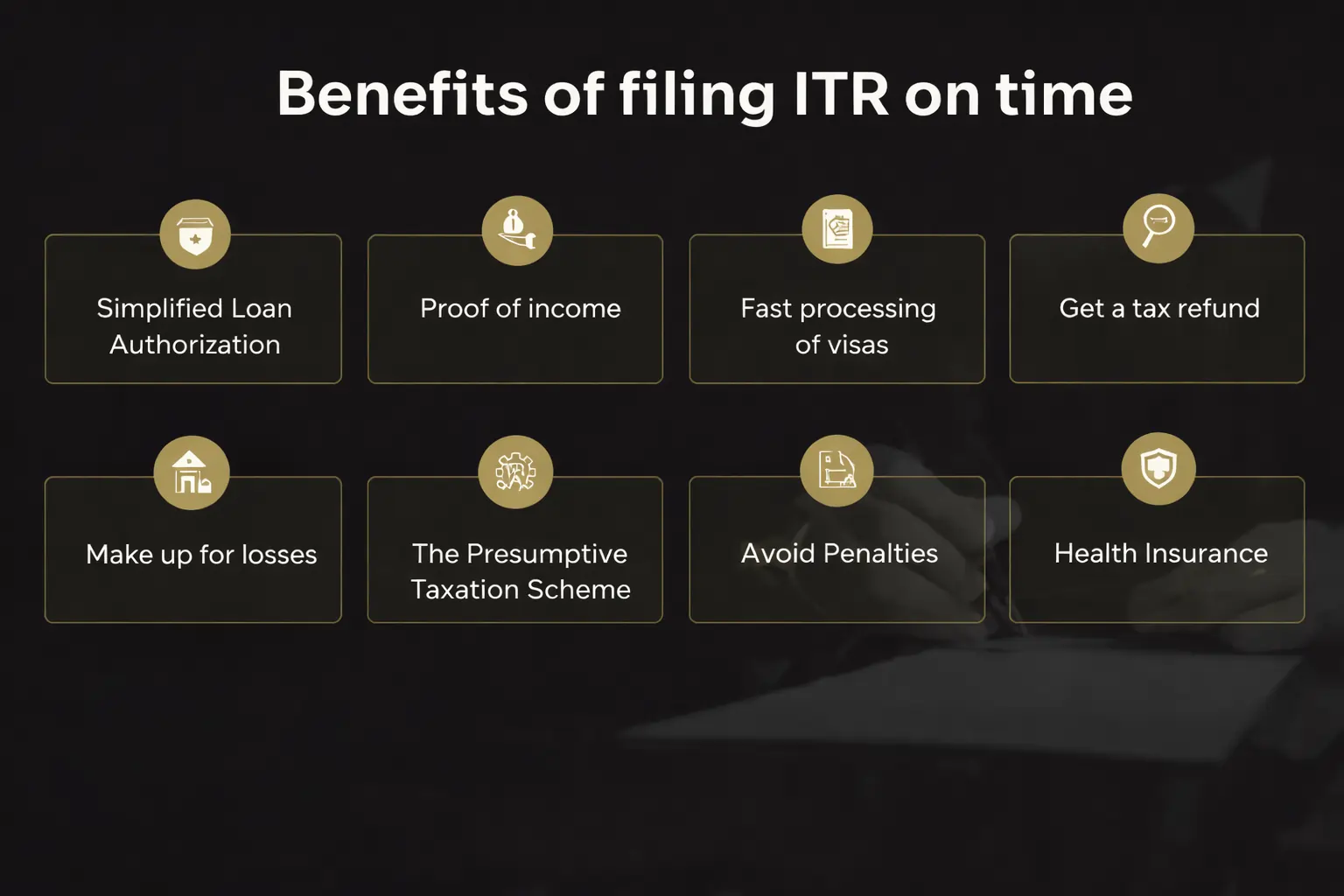

Benefits of Filing ITR on Time

Filing an ITR helps you to claim tax deductions, thus reducing your tax outgo and growing your savings. Here are some more benefits of filing the tax return on time-

1. Simplified Loan Authorization

The financial stability of borrowers is essential for lenders. Borrowers are required to provide an Income Tax Return (ITR) for a minimum of three consecutive years when applying for a loan. So. It's important to file the return on time.

2. Proof of Income

Another great thing about submitting an ITR is that it may be used as proof of income. The ITR is one of the most generally accepted cash proofs because it has extensive information about your yearly income and the taxes you've paid. So, if you have to provide proof of income somewhere, file the ITR and send in the receipt as proof.

3. Fast Processing of Visas

International embassies need to know the applicant's income and tax situation. So, if you want to go to another country and are about to apply for a visa, the embassy will mostly want your ITR so they can quickly check your income and tax status.

4. Get a Tax Refund

Claiming tax refunds is another huge benefit of completing an income tax return. If you've paid more in income tax than you owe, you can file a tax return to get your money back. After verification, the tax department will deposit the refund amount directly into your bank account.

5. Make Up For Losses

Any business can lose money in a certain financial year. If you own a business, you can file an ITR to make up for the loss. The ITR process lets you carry over losses to the next year. But this payment for losses is only feasible if the ITR is filed on time.

6. The Presumptive Taxation Scheme

One of the perks of submitting an ITR is that you can get a Presumptive Taxation Scheme. The Income Tax Act says that self-employed people and professionals must keep regular books of account and have them audited. Small taxpayers can avoid this tedious labor by choosing the Presumptive Taxation Scheme. This lets self-employed people report their income at a set rate when they file their ITR.

7. Avoid Penalties

As we said at the start, filing your ITR late could lead to fines. You may avoid these kinds of fines and other negative outcomes by filing your taxes on time every year.

8. Health Insurance

Taxpayers can get a tax break of up to INR 25,000 in a financial year for premiums paid on a health insurance plan under Section 80D of the IT Act. Senior persons can get higher deduction limitations. One of the best things about ITR is that it lets people take deductions for their medical insurance.

ITR Submission Errors: How to Correct Them?

Filing a revised return (Section 139(5)). If you missed any addition of income, or deductions, or made any calculation errors, you can file a revised return. The deadline for filing is before 31st December of the relevant assessment year. There is no limit to the number of times you can revise a return.

You can refile the ITR by going to the income tax portal, then navigate to ‘Services’, then click on rectification. After that, if you haven’t verified the return and there are some errors, you can use the ‘discard’ option to delete the unverified return and file a fresh one.

If you don’t correct the errors, such as missed income or any wrong deductions, the Income Tax Department can send you a notice. A refund could be delayed, and there may be some penalties you have to pay.

👉 Read More: Old Tax Regime vs New Tax Regime

Avoid These Mistakes to File Your ITR on Time

Most delays happen due to simple misunderstandings. Below are the most common mistakes taxpayers make regarding the last date to file ITR:

Assuming everyone has the same deadline: Many taxpayers think 31 July is the last ITR filing date. The deadline depends on whether you are a paid employee, a business owner requiring audit, or covered by transfer pricing. Unintentional late filing can result from not verifying your due date.

Watching for deadline extensions: Some delay submitting hoping the government will extend the deadline. Extensions have happened, but not every year. If no extension is granted, last-minute stress or late fees may follow.

Thinking “No tax payable” equals no filing: A popular myth is that you don't need to submit an ITR if your tax burden is zero due to TDS or deductions. If your income exceeds the basic exemption limit, you must file. Avoiding filing can delay refunds and cause notices.

Confusing FY and AY: Taxpayers often file the wrong year. Income is earned in the Financial Year and taxed in the Assessment Year. Mistaking FY for AY typically leads to missing the filing window.

Not Paying Advance Taxes: Some taxpayers believe they are safe if they file before the deadline. Even if the return is filed on time, Sections 234B and 234C interest may apply if advance tax was not paid properly during the year.

Waiting for the last date: Final filing raises the likelihood of technical issues, online traffic issues, OTP delays, and banking errors. If you miss the deadline one day, late filing fees and interest may apply.

Not checking the ITR after filing: Verifying the return within the deadline is required. Numerous taxpayers forget to E-Verify or send an ITR-V, invalidating the return as never filed.

Failure to check Form 26AS and AIS before filing: Not reconciling income facts with Form 26AS or the Annual Information Statement might lead to inaccurate reporting. Later discrepancies may require adjustment or notices.

Assuming late return has no major effects: Some people believe filing late incurs a modest cost. Late filing can cause loss of carry- forward losses, unpaid tax interest, and compliance concerns.

Not taking professional help: There are many steps to filing the ITR, and many people can make mistakes and may file it incorrectly, so consulting a CA professional who can file it properly is important.

How DigiLawyer Helps You File Returns Before the Last Date

- Share Your Details & Documents Quickly: Upload your PAN, Aadhaar, Form 16, and other required documents without hassle.

- Expert CA Review Before Deadline: Our experienced CAs review your income details, calculate your tax liability, and ensure all eligible deductions are claimed before the due date.

- Accurate & Timely ITR Filing: We file your Income Tax Return on the government portal well before the last date to avoid penalties and late fees.

- Acknowledgement & E-Verification Support: Get your ITR acknowledgement instantly and complete e-verification smoothly with our step-by-step guidance.

- Refund Tracking & Post-Filing Assistance: Track your refund status easily and receive continued support even after filing is completed.

👉 Read More: Income Tax Return Filing Without Form 16

Conclusion

Filing your ITR before the last date is not just about avoiding a ₹5,000 penalty or 1% monthly interest; it is about protecting your financial credibility, securing refunds on time, and maintaining a clean compliance record. Whether you are a salaried employee, a business owner, or a professional, understanding your correct due date and filing accurately can save you from unnecessary stress, notices, and financial loss. Waiting until the last moment increases the risk of mistakes, technical glitches, and missed deductions that can cost you much more in the long run.

With DigiLawyer, you don’t have to worry about deadlines, penalties, or complex tax calculations. Our expert CAs ensure accurate filing, proper deduction claims, and complete compliance all before the due date. From document review to e-verification and refund tracking, we handle the entire process smoothly so you can stay stress-free. Don’t wait for the last date rush. File your ITR confidently and on time with DigiLawyer today

FAQs

What is the difference between original due date, belated return, and updated return?

The original due date is the standard deadline (e.g., 31st July 2026 for most individuals). A belated return can be filed after the due date but before 31st December 2026 with penalties. An updated return can be filed within 4 years from the end of the relevant assessment year, but additional tax and restrictions apply.

Will the government extend the last date to file ITR in 2026?

ITR deadlines are extended only in special situations, such as technical glitches or large-scale issues. However, extensions are not guaranteed every year. Taxpayers should not rely on possible extensions and should file before the original due date.

What if I miss the ITR deadline by just one day?

Even a one-day delay can attract:

- Late filing fees under Section 234F

- Interest under Section 234A The system automatically calculates penalties once the due date passes.

Do I need to file ITR if my income is below ₹2.5 lakh?

If your total income is below the basic exemption limit, filing is generally not mandatory. However, filing voluntarily may help in:

- Claiming tax refunds

- Maintaining financial records

- Visa or loan applications

Can I file ITR without Form 16 before the last date?

Yes, you can file ITR without Form 16 by using:

- Salary slips

- Form 26AS

- Annual Information Statement (AIS) However, accurate reconciliation is important to avoid notices.

What happens if I forget to e-verify my ITR before the deadline?

If you fail to e-verify within the prescribed time limit, your return may be treated as invalid, meaning it will be considered as not filed at all. This can lead to penalties and compliance issues.

How long does it take to receive a tax refund after filing ITR on time?

If your ITR is filed correctly and verified promptly, refunds are generally processed within a few weeks. Delays may occur if there are discrepancies or late filing.

Can salaried employees receive a notice even after filing ITR before the due date?

Yes, notices may be issued if:

- Income details mismatch with AIS/26AS

- Deductions are incorrectly claimed

- High-value transactions are not reported Filing on time reduces risk, but accuracy is equally important.

Is advance tax related to the ITR filing deadline?

Yes. Even if you file before the due date, failure to pay proper advance tax during the financial year can attract interest under Sections 234B and 234C.

- Introduction

- What Is the Deadline For Filing Income Tax Return (FY 2025-2026)?

- What Happens If You Miss the Due Date to File ITR

- 1. Late filing fees (Section 234F)

- 2. Interest on Tax Due (Section 234A)

- 3. Risk of Notice from the Income Tax Department

- What Is the Next Step to Take If You Miss the Deadline?

- Consequences of Missing the ITR Filing Deadline

- Benefits of Filing ITR on Time

- 1. Simplified Loan Authorization

- 2. Proof of Income

- 3. Fast Processing of Visas

- 4. Get a Tax Refund

- 5. Make Up For Losses

- 6. The Presumptive Taxation Scheme

- 7. Avoid Penalties

- 8. Health Insurance

- ITR Submission Errors: How to Correct Them?

- Avoid These Mistakes to File Your ITR on Time

- How DigiLawyer Helps You File Returns Before the Last Date

- Conclusion

- FAQs

How to Claim HRA While Filing ITR: Eligibility, Calculation & Documents

Learn how to claim HRA correctly, calculate your exemption, prepare the required documents, and avoid common mistakes when filing your Income Tax Return.

Difference Between Tax Evasion, Tax Avoidance and Tax Planning

Tax planning, tax avoidance, and tax evasion may sound similar, but their legality and consequences are completely different. Here’s a simple breakdown of what is legal, risky, and illegal.

5 Ways to Save Income Tax in New Tax Regime (FY 2025-26)

The new tax regime offers lower tax rates, but saving money now depends on your salary structure. Here’s what you need to know to reduce your tax.

Disclaimer: DigiLawyer is not a law firm, a substitute for a lawyer or law firm, a chartered accountancy firm, or a company secretary firm. We act solely as an intermediary between users and registered professionals, and also offer AI-powered legal assistance, consultation, and document drafting tools to improve access to legal support. Use of our website, services, or AI tools is at the sole risk of the user and does not create any lawyer-client or professional relationship. All consultations and interactions facilitated through our platform are strictly between the user and independent professionals. DigiLawyer is not liable for any actions, decisions, or outcomes arising from the use of our platform, AI tools, or reliance on any advice, consultation, or content provided by us or third-party professionals.

Use of our products and services is subject to our Privacy Policy & Terms of Service