Old Tax Regime vs New Tax Regime 2026: Which One Should You Choose?

60-Second Summary

- Both tax regimes exist in FY 2025-26 (AY 2026-27). The new regime is the default. You must actively opt out.

- New regime: Zero tax up to Rs. 12 lakh (Rs. 12.75 lakh for salaried). Lower rates. No major deductions.

- Old regime: Higher rates but big deductions. Good if you invest heavily in 80C, 80D, home loans, and NPS.

- The crossover point for most salaried employees is approximately Rs. 3.75 lakh in total annual deductions.

- Budget 2026 made no changes to tax slabs. What was announced in Budget 2025 continues.

- Salaried employees can switch regimes every year at the ITR filing. Business owners have limited switching rights.

Bottom line: Run the numbers. Both regimes are valid. The right one depends entirely on your situation.

Why Choosing the Right Tax Regime Matters in 2026 ?

Every April, millions of Indian taxpayers fill in their investment declarations, submit HRA proof to HR, and file their ITR. Most people do it by habit. A surprising number of them end up paying more tax than they legally need to. Not because they missed the deadline. Because they picked the wrong regime without doing the math.

Here is the most important thing to understand first: the government is not neutral between the two regimes. Since FY 2024-25, the new tax regime has been the default. If you do nothing, you get slotted into it automatically. If you want the old regime with its deductions and exemptions, you have to actively choose it.

So what does that mean for you? It means inertia now costs you money if you are someone with heavy investments, a home loan, and significant insurance premiums. The new regime suits a different kind of taxpayer. The question is which kind you are.

This guide breaks it all down. We cover the FY 2025-26 (AY 2026-27) tax slabs under both regimes, the deductions that still matter, a worked example with real numbers, and a step-by-step framework for choosing. Budget 2026 confirmed no changes to slab rates, so everything you read here applies directly to this financial year. Once you’ve figured out your slabs and deductions, it’s also important to know which ITR form fits your situation, as the right choice makes filing much simpler.

One quick clarification before we dive in: FY 2025-26 means the year your income is earned (April 2025 to March 2026). AY 2026-27 is when you file your return and get assessed. When your CA says 'AY 2026-27', they are talking about your income from this year.

Understanding the Two Tax Regimes

Think of the two regimes as two different pricing menus at a restaurant. One menu (old regime) has higher base prices but lets you use coupons, loyalty points, and discount vouchers. The other (new regime) has lower base prices but does not accept any coupons at all. Which one is better for you depends entirely on how many valid coupons you are carrying.

➤ The Old Tax Regime: The Deductions Playground

The old regime has been around since the Income Tax Act of 1961. It offers higher tax rates but allows you to significantly reduce your taxable income through a long list of deductions and exemptions. If you have a home loan, pay rent, invest in PPF or ELSS, buy health insurance, and contribute to NPS, the old regime can carve a large chunk off your taxable income before you pay a single rupee of tax.

The flipside is complex. You need to track investments, submit proof to your employer, reconcile exemptions, and maintain documentation. This is the regime that made tax season stressful.

➤ The New Tax Regime: The Simplicity-First Approach

Introduced in 2020 and progressively sweetened since then, the new regime trades deductions for lower base rates. Budget 2025 made it considerably more attractive by raising the tax-free limit to Rs. 12 lakh (via Section 87A rebate) and increasing the standard deduction for salaried taxpayers to Rs. 75,000.

The result a salaried employee earning Rs. 12.75 lakh per year pays zero income tax under the new regime. Zero. That was simply not possible in the old regime without very disciplined investment planning.

Budget 2026, presented by Finance Minister Nirmala Sitharaman on 1 February 2026, kept all these slab rates and provisions unchanged. The new regime remains the default, and the slabs from Budget 2025 continue to apply for AY 2026-27, including how income tax notices affect salaried employees.

One thing that surprises many people: the new regime is not just for young earners with no investments. Even someone with some 80C investments might find the new regime better at certain income levels. The only way to know is to calculate both. For professional guidance, consider an online CA consultation before filing

Income Tax Slabs for FY 2025-26 (AY 2026-27)

Let us start with the most referenced information in any tax guide, the actual numbers. Both regimes use a progressive slab system, meaning you pay different rates on different portions of your income, not one flat rate on the whole amount.

➤ New Regime Income Tax Slabs FY 2025-26 (AY 2026-27)

One structural change in the new regime that many overlook is that it applies the same slabs to all ages. A 70-year-old retiree and a 25-year-old employee face identical rates under the new regime, unlike the old system where age-based exemptions applied, as explained in the new salary rules for 2025.

Annual Income Range | Tax Rate |

Up to Rs. 4,00,000 | Nil |

Rs. 4,00,001 to Rs. 8,00,000 | 5% |

Rs. 8,00,001 to Rs. 12,00,000 | 10% |

Rs. 12,00,001 to Rs. 16,00,000 | 15% |

Rs. 16,00,001 to Rs. 20,00,000 | 20% |

Rs. 20,00,001 to Rs. 24,00,000 | 25% |

Above Rs. 24,00,000 | 30% |

Important: Add 4% Health and Education Cess on your total tax liability under both regimes. Surcharge applies on income above Rs. 50 lakh (10%), Rs. 1 crore (15%), Rs. 2 crore (25% under the new regime, capped lower than old regime).

👉Section 87A Rebate (New Regime): If your taxable income is Rs. 12 lakh or below, your entire tax liability is rebated. Combined with the Rs. 75,000 standard deduction for salaried individuals, this makes income up to Rs. 12.75 lakh effectively tax-free.

➤ Old Regime Income Tax Slabs FY 2025-26 (AY 2026-27)

The old regime has different slabs for different age groups. This is one genuine advantage for senior citizens, who get a higher basic exemption. The slabs themselves have not changed in years.

Annual Income Range | Tax Rate |

Up to Rs. 2,50,000 | Nil |

Rs. 2,50,001 to Rs. 5,00,000 | 5% |

Rs. 5,00,001 to Rs. 10,00,000 | 20% |

Above Rs. 10,00,000 | 30% |

Your tax-free income limit depends on your age (under the old regime). Here’s how it breaks down:

Category | Basic Exemption Limit (Old Regime Only) |

Below 60 years | Rs. 2,50,000 |

Senior Citizen (60-80 years) | Rs. 3,00,000 |

Super Senior Citizen (80+years) | Rs. 5,00,000 |

👉 Section 87A Rebate (Old Regime): Tax rebate up to Rs. 12,500 for taxable income up to Rs. 5 lakh. Standard deduction of Rs. 50,000 for salaried taxpayers. Much lower thresholds than the new regime.

Major Differences Between the Old and New Regimes

The headline numbers are just the start. The real differences show up in how each regime treats your money, your investments, and your compliance burden.

Parameter | Old Tax Regime | New Tax Regime |

Default Status | Optional (must actively choose) | Default (automatic from FY 2024-25) |

Basic Exemption | Rs. 2.5L / 3L / 5L (age-based) | Rs. 4,00,000 (all ages, uniform) |

Standard Deduction | Rs. 50,000 (salaried) | Rs. 75,000 (salaried) |

Section 80C | Up to Rs. 1,50,000 | Not available |

Section 80D (Health) | Up to Rs. 25,000 / 50,000 | Not available |

HRA Exemption | Available | Not available |

Home Loan Interest (24b) | Up to Rs. 2,00,000 | Only for let-out property |

NPS (80CCD(1B)) | Additional Rs. 50,000 | Not available (only employer contribution 80CCD(2)) |

Section 87A Rebate | Up to Rs. 12,500 (income <= Rs. 5L) | Up to Rs. 60,000 (income <= Rs. 12L) |

Max Surcharge | 37% (income > Rs. 5 crore) | 25%(capped, better for very high earners) |

ITR Complexity | Higher (many proofs/declarations) | Lower (fewer documents) |

Switching Frequency | Salaried: yearly at ITR filing | Default; opt out via Form 10IEA if needed |

Important Deductions to Know Under the Old Regime

If you are evaluating whether the old regime makes sense for you, these are the provisions that actually move the needle. The question is not whether these sections exist. It is whether you are already using them, or are willing to.

➤ Section 80C: The Rs. 1.5 Lakh Workhorse

Section 80C allows a deduction of up to Rs. 1,50,000 per year for a wide range of investments and expenses. This is the most commonly used deduction in India. What qualifies:

- PPF (Public Provident Fund) contributions

- Employee PF contributions (EPF, if not already excluded from taxable income)

- ELSS mutual fund investments (Equity Linked Savings Scheme)

- Life insurance premium payments

- 5-year tax-saving fixed deposits

- Tuition fees for children (up to 2 children)

- Principal repayment on the home loan

- NSC (National Savings Certificate), ULIP, SCSS

The crucial point: most salaried employees with EPF contributions and LIC policies are already partially or fully using their 80C limit without deliberate planning. If you are contributing Rs. 1.5 lakh or more per year across these instruments, including your EPF contributions, you may already be maximizing this deduction, making proper PF return filing essential to ensure compliance and accurate reporting.

➤ Section 80D: Health Insurance Deduction

Section 80D offers a deduction for health insurance premiums paid for yourself, spouse, children, and parents. The limits are:

- Self + family (below 60 years): Rs. 25,000

- If self or family is a senior citizen: Rs. 50,000

- Additionally: Rs. 25,000 for parents (Rs. 50,000 if parents are senior citizens)

- Maximum possible deduction under 80D: Rs. 1,00,000 (Rs. 50,000 for self as senior + Rs. 50,000 for senior parents)

➤ HRA (House Rent Allowance) Exemption

If you live in rented accommodation and receive HRA as part of your salary, you can claim an exemption. The exemption is the minimum of three calculations:

- Actual HRA received from employer

- 50% of basic salary (metro) or 40% of basic salary (non-metro)

- Actual rent paid minus 10% of basic salary

This can be a very large deduction for people in expensive cities like Mumbai, Delhi, or Bengaluru paying significant rent. A person paying Rs. 30,000 per month in rent in Delhi could exempt Rs. 2.5 to 3.5 lakh annually from tax. This alone often tips the balance toward the old regime for metro renters.

👉 Read More About the New Rent Rules 2026

➤ Home Loan Benefits (80C + Section 24b)

Home loan borrowers get a double benefit under the old regime. Principal repayment goes toward the Rs. 1.5 lakh 80C limit. Interest paid on a self-occupied property is deductible separately under Section 24b up to Rs. 2,00,000. Combined, a home loan of Rs. 50 lakh could generate Rs. 3.5 lakh or more in annual deductions.

➤ NPS (Section 80CCD(1B)): The Hidden Extra Rs. 50,000

Over and above the Rs. 1.5 lakh 80C limit, contributing to NPS (National Pension System) gives you an additional deduction of up to Rs. 50,000 under Section 80CCD(1B). This is available only under the old regime. It is one of the most underused deductions in India.

At a 30% tax bracket, this single deduction saves you Rs. 15,000 + cess annually. If you are in the old regime and are not using 80CCD(1B), you are probably leaving money on the table.

➤ Section 80E: Education Loan Interest

Interest paid on a loan taken for higher education is deductible with no upper limit for up to 8 years. This is available only under the old regime. For someone with a substantial education loan, this deduction alone could justify staying in the old regime during their repayment years.

One practical note: if you have recently taken an education loan and are unsure about how to structure your repayments and claims for maximum benefit, speaking with a tax expert early in the year can save significant money.

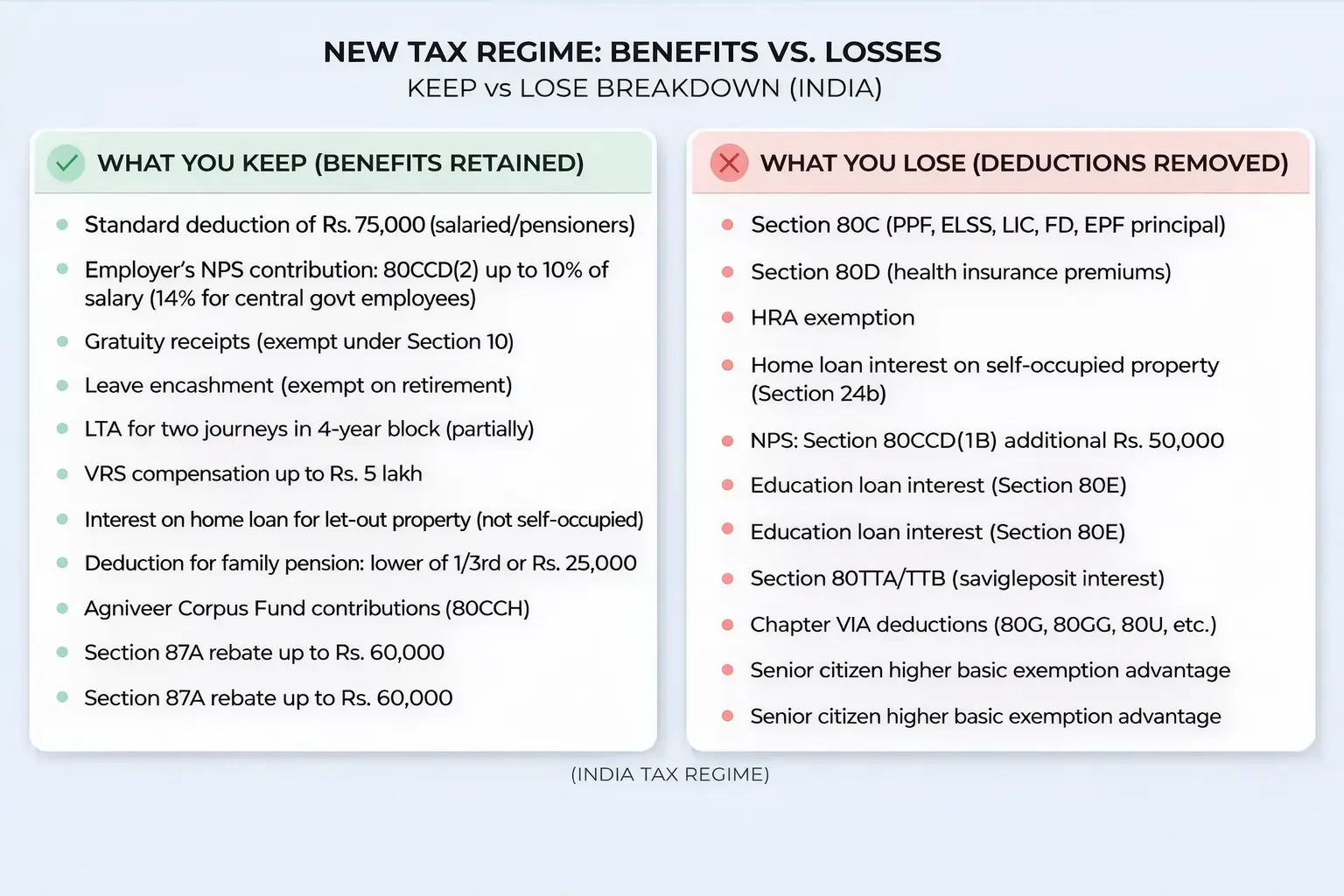

What is Actually Allowed Under the New Regime

The new regime strips out most deductions, but it is not entirely bare. A few provisions survive. Understanding these helps you see the full picture before deciding.

One nuance that often goes unnoticed: the employer's NPS contribution under 80CCD(2) is a deduction even under the new regime. If your employer is willing to restructure your CTC to route more salary through NPS contribution, this is a legitimate tax-saving lever under the new regime. Not many employees know to ask for this.

How to Choose the Right Regime: A Step-by-Step Framework

Stop guessing. Here is the actual method.

- Start with your gross income: annual CTC minus any employer-side costs. For salaried, this is your total salary from Form 16 Part B.

- List every deduction you will genuinely claim: not aspirational investments, but actual ones. 80C investments you have already made, health insurance you actually pay, rent receipts you have, and home loan statements.

- Calculate old regime tax: subtract all deductions and exemptions from gross income, apply old regime slabs, and add 4% cess.

- Calculate new regime tax: subtract only standard deduction (Rs. 75,000 for salaried), apply new regime slabs, check 87A rebate eligibility (income under Rs. 12 lakh), add 4% cess.

- Compare the two final numbers. Pick whichever is lower. That is your regime for this year.

- One more check: if you are within Rs. 5,000-10,000 of the old regime being better, factor in compliance effort. Is it worth maintaining all the documentation for a small saving?

The decision point shifts with income. At Rs. 8 lakh, the new regime almost always wins even with a moderate 80C. At Rs. 15 lakh with a home loan and HRA, the old regime frequently wins. At Rs. 25 lakh with no deductions, the new regime wins decisively.

👉 Read More: How to File Income Tax Return Without Form 16

Sample Tax Calculation: Who Actually Pays Less?

Forget theory, let’s see a real example.

Here is Arjun. He is 34 years old, working as a senior analyst in Bengaluru, earning Rs. 10 lakh per year. He pays Rs. 18,000 per month in rent and has made the following investments this year:

- EPF + ELSS+ LIC premium: Rs. 1,50,000 (80C fully used)

- Health insurance (Self + Family): Rs. 25,000 (80D)

- HRA exemption (metro): Rs. 1,20,000 (calculated from salary structure)

- Total deductions: Rs. 2,95,000 + Rs. 50,000 standard deduction = Rs. 3,45,000

Step | Old Regime | New Regime |

Gross Income | Rs. 10,00,000 | Rs. 10,00,000 |

Standard Deduction | Rs. 50,000 | Rs. 75,000 |

Other Deductions (80C, 80D, HRA) | Rs. 2,95,000 | Nil |

Taxable Income | Rs. 6,55,000 | Rs. 9,25,000 |

Tax on Slabs (before cess) | Rs. 42,500 | Rs. 52,500 |

4% Cess | Rs. 1,700 | Rs. 2,100 |

Section 87A Rebate | Nil (income > Rs. 5L) | Nil (income > Rs. 12L; rebate does not apply) |

Total Tax Payable | Rs. 44,200 | Rs. 54,600 |

Savings vs. the other | SAVE Rs. 10,400 | PAY Rs. 10,400 more |

Arjun saves Rs. 10,400 per year by choosing the old regime. But here is what changes the picture: if Arjun's EPF is already included in his 80C and his LIC lapses next year, his deductions drop to Rs. 1.75 lakh. Re-run the calculation and the new regime comes out ahead.

This is precisely why the regime choice should not be a one-time decision. It deserves a fresh look every April.

👉Marginal Relief Note: If your income is just above Rs. 12 lakh (say Rs. 12.5 lakh) under the new regime, tax does not jump dramatically. Marginal relief ensures that the tax you pay on the income above Rs. 12 lakh never exceeds the incremental income itself. So crossing Rs. 12 lakh slightly does not mean you suddenly owe Rs. 60,000 in taxes.

Important Tax Deadlines for FY 2025-26

Miss a deadline and you are not just paying interest. You lose the ability to revise your return, claim certain deductions, and sometimes even offset losses against future income.

Deadline | Date | What It Covers |

Advance Tax (1st) | 15 June 2025 | 15% of the estimated annual tax liability |

Advance Tax (2nd) | 15 September 2025 | 45% of estimated annual tax liability (cumulative) |

Advance Tax (3rd) | 15 December 2025 | 75% of estimated annual tax liability (cumulative) |

Advance Tax (4th) | 15 March 2026 | 100% of estimated annual tax liability (cumulative) |

ITR Filing Deadline | 31 July 2026 | For individuals and non-audit business cases (Budget 2026 confirmed same date) |

ITR Filing (Audit Cases) | 31 October 2026 | Businesses requiring a tax audit |

Belated / Revised ITR | 31 December 2026 | Last date to file late or revise a filed return for AY 2026-27 |

Investment Proof to Employer | January/February 2026 | For TDS recalculation, it varies by employer |

Budget 2026 also introduced a significant change to revised returns: taxpayers can now revise returns up to 31 March of the following year by paying a nominal fee. This extends the window for corrections beyond the earlier December deadline in some cases. Always verify the latest notification from CBDT before relying on this.

👉 Read More: Last Date to File ITR

How DigiLawyer Simplifies Tax Season for You

Tax season should not be stressful. And yet, for most people, it involves a combination of frantic last-minute calculations, half-remembered investment amounts, and anxiety about whether they picked up the right regime.

DigiLawyer exists to change that. We bring together tax experts, CAs, and legal professionals on our platform so that individual taxpayers and business owners can make informed decisions without needing a full-time finance team.

Regime Comparison &Tax Planning: We calculate your liability under both regimes with your actual numbers and tell you exactly which one to choose.

ITR Filing with Expert CA Support: Our CAs handle your complete ITR filing, capital gains schedules, and regime selection, all reviewed before submission.

Tax Notice Response & Resolution: Received a notice from the income tax department? Our team drafts the response, communicates with authorities, and resolves it.

Frequently Asked Questions on Tax Regime 2026

Can I switch between the old and new tax regimes every year?

Salaried employees without business income can switch every year when filing their ITR, regardless of what they declared to their employer. Business owners, however, have restricted switching rights and must generally file Form 10IEA to opt out of the default new regime.

Which regime is better for a salary of ₹7 lakh?

The new regime results in zero tax due to the Section 87A rebate. The old regime also allows for zero tax, but only if you claim full deductions (like ₹1.5 lakh under 80C). The new regime is usually the winner here for its simplicity.

Do freelancers benefit from staying in the old regime?

It depends on your personal deductions. Freelancers first deduct business expenses (rent, tech, internet) from their gross income. If you also have high personal deductions like a home loan or life insurance, the old regime might save you more. Otherwise, the new regime is often easier.

Is tax planning completely legal?

Yes. Tax planning, using legal provisions like 80C or choosing a specific regime, is encouraged. It is different from tax evasion (e.g., filing fake HRA receipts), which is illegal. Using the law to minimize your liability is perfectly safe.

What is the Income Tax Act 2025?

It is a simplified version of the 1961 Act. While it takes effect on April 1, 2026, it does not change your tax liability for AY 2026-27 (income earned in FY 2025-26). The old rules still apply for this filing season.

Can I claim both HRA and a home loan deduction?

Yes, if the situation is genuine, for example, you rent in the city where you work but own a home in your hometown. Keep solid documentation, including rent receipts and loan statements, to support this during any potential audit.

Disclaimer: This blog is for informational purposes only and does not constitute legal or financial advice. Tax laws are subject to change. Always verify current provisions with a qualified CA or tax professional before making financial decisions. All figures in this article are based on the Finance Act applicable to FY 2025-26 (AY 2026-27) as confirmed by Union Budget 2026.

”- Why Choosing the Right Tax Regime Matters in 2026 ?

- Understanding the Two Tax Regimes

- ➤ The Old Tax Regime: The Deductions Playground

- ➤ The New Tax Regime: The Simplicity-First Approach

- Income Tax Slabs for FY 2025-26 (AY 2026-27)

- ➤ New Regime Income Tax Slabs FY 2025-26 (AY 2026-27)

- ➤ Old Regime Income Tax Slabs FY 2025-26 (AY 2026-27)

- Major Differences Between the Old and New Regimes

- Important Deductions to Know Under the Old Regime

- ➤ Section 80C: The Rs. 1.5 Lakh Workhorse

- ➤ Section 80D: Health Insurance Deduction

- ➤ HRA (House Rent Allowance) Exemption

- ➤ Home Loan Benefits (80C + Section 24b)

- ➤ NPS (Section 80CCD(1B)): The Hidden Extra Rs. 50,000

- ➤ Section 80E: Education Loan Interest

- What is Actually Allowed Under the New Regime

- How to Choose the Right Regime: A Step-by-Step Framework

- Sample Tax Calculation: Who Actually Pays Less?

- Important Tax Deadlines for FY 2025-26

- How DigiLawyer Simplifies Tax Season for You

- Frequently Asked Questions on Tax Regime 2026

Disclaimer: DigiLawyer is not a law firm, a substitute for a lawyer or law firm, a chartered accountancy firm, or a company secretary firm. We act solely as an intermediary between users and registered professionals, and also offer AI-powered legal assistance, consultation, and document drafting tools to improve access to legal support. Use of our website, services, or AI tools is at the sole risk of the user and does not create any lawyer-client or professional relationship. All consultations and interactions facilitated through our platform are strictly between the user and independent professionals. DigiLawyer is not liable for any actions, decisions, or outcomes arising from the use of our platform, AI tools, or reliance on any advice, consultation, or content provided by us or third-party professionals.

Use of our products and services is subject to our Privacy Policy & Terms of Service